Asia Pacific Healthcare and Social Services Market Size, 2033

Asia Pacific Healthcare and Social Services Market Size

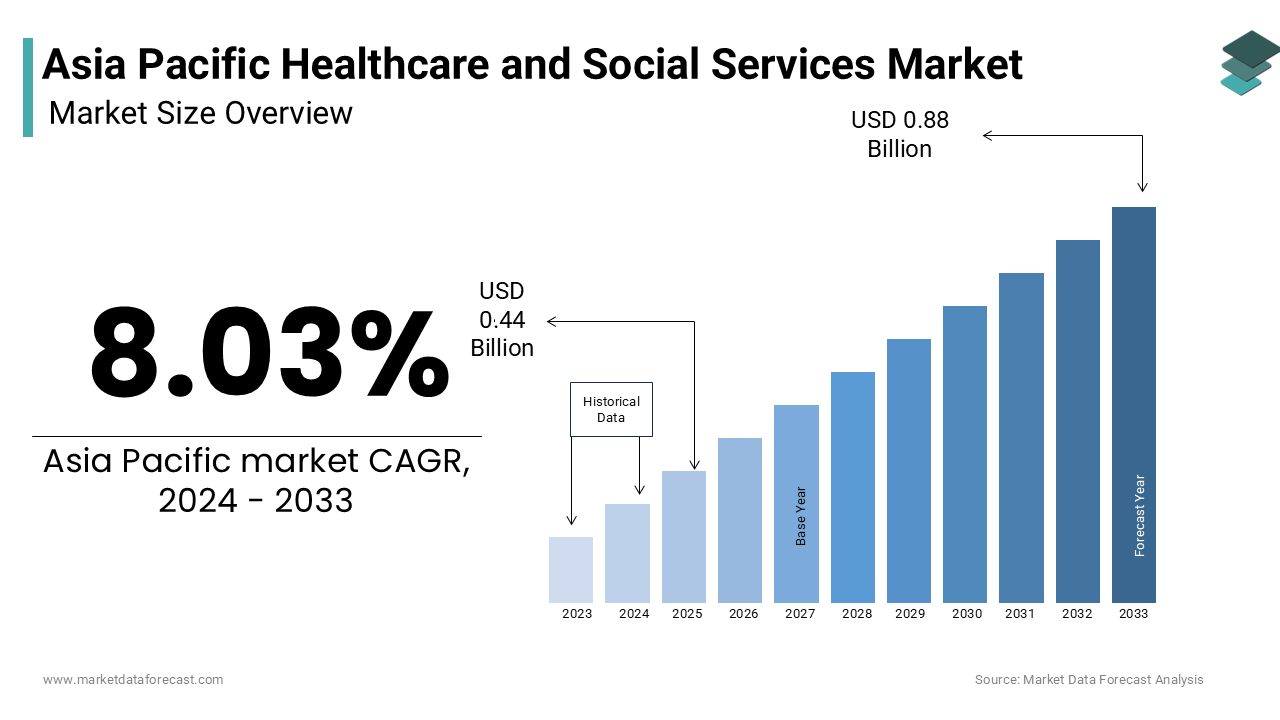

The Asia Pacific Healthcare and Social Services Market Size is anticipated to rise from USD 0.44 billion in 2024 to USD 0.88 billion in 2033, growing at a CAGR of 8.03%.

Healthcare and social services are medical, preventive, rehabilitative, and community-based support systems designed to meet the evolving health and welfare needs of populations across diverse economies. Characterized by stark contrasts between advanced urban healthcare infrastructure and under-resourced rural regions, the sector is shaped by demographic shifts, government policy reforms, and rising public expectations. According to the World Health Organization, life expectancy in the region has increased by nearly 7 years between 2000 and 2022, reaching an average of 74.5 years, reflecting improvements in disease management and maternal health. However, disparities persist: as per the United Nations Economic and Social Commission for Asia and the Pacific, over 60% of the region’s population lacks access to essential social protection services, including long-term care and disability support. Countries such as Japan and Australia exhibit mature, integrated health-social service models, while nations like Cambodia and Papua New Guinea rely heavily on donor-funded programs and informal caregiving networks.

MARKET DRIVERS

Rapid Aging of the Population and Rising Demand for Long-Term Care

The aging demographic across the Asia Pacific region is fundamentally reshaping the demand for integrated healthcare and social services. According to the United Nations, the number of individuals aged 65 and over in the region is projected to reach 693 million by 2050, more than doubling from 2020 levels, with Japan, South Korea, and Thailand leading this transition. In Japan, people aged 65+ already constitute 29.1% of the total population, the highest proportion globally, as per the Ministry of Health, Labour and Welfare. This shift has intensified the need for geriatric care, home-based nursing, and assisted living facilities. Countries are responding with policy reforms: Japan’s Long-Term Care Insurance system, established in 2000, now supports over 6.5 million beneficiaries, serving as a model for emerging programs in Singapore and Malaysia. The expansion of community-based care networks and investment in eldercare infrastructure are now central to national health strategies.

Expansion of Universal Health Coverage and Social Protection Reforms

Governments across the Asia Pacific are increasingly prioritizing equitable access to healthcare and social support through institutionalized coverage programs. According to the World Health Organization, 18 countries in the region have implemented or expanded universal health coverage (UHC) initiatives since 2010, including Indonesia’s Jaminan Kesehatan Nasional (JKN) and India’s Ayushman Bharat scheme. Indonesia’s JKN, launched in 2034, enrolled 248 million people, covering nearly 84% of the population, as confirmed by the National Health Insurance Agency (BPJS). These systems integrate medical care with preventive and rehabilitative services, often extending into community health centers and social outreach programs. In Thailand, the Universal Coverage Scheme ensures access to primary care for 48 million citizens, supported by a network of 10,000 health promotion hospitals.

MARKET RESTRAINTS

Severe Shortage of Trained Healthcare and Social Work Professionals

A critical bottleneck in the Asia Pacific healthcare and social services sector is the insufficient supply of qualified personnel. According to the World Health Organization, the region faces a deficit of over 1.7 million nurses and 600,000 doctors, with rural and remote areas disproportionately affected. In India, the doctor-to-patient ratio stands at 1:1,457, far below the WHO-recommended 1:1,000, as per the Indian Medical Association. Similarly, social work remains an underdeveloped profession: Australia, a regional leader, has approximately 110,000 registered social workers, while Indonesia, with a population of 275 million, has fewer than 5,000 certified practitioners, according to the International Federation of Social Workers. Training programs are limited, and career pathways are often poorly defined, discouraging workforce entry. As per the Asian Development Bank, 12 countries in the region lack formal accreditation systems for social care workers, undermining service quality and scalability. This human resource gap constrains the delivery of both clinical and psychosocial support services.

Fragmented Integration Between Healthcare and Social Service Systems

Despite growing recognition of the need for holistic care, institutional silos between medical and social service providers persist across much of the Asia Pacific. As per the OECD, only five countries in the regionAustralia, Japan, New Zealand, South Korea, and Singapore, have established formal mechanisms for cross-sector coordination between health and social welfare agencies. In many nations, patients transitioning from hospital to home care face discontinuities due to incompatible data systems and misaligned funding streams. The lack of integrated care models leads to higher readmission rates and increased burden on informal caregivers, who number over 250 million across the region, as per the United Nations. Without unified governance frameworks and shared care protocols, service delivery remains inefficient and patient outcomes suffer.

MARKET OPPORTUNITIES

Digital Health Platforms Bridging Clinical and Social Care Gaps

The proliferation of digital technologies presents a transformative opportunity to integrate healthcare with social services across the Asia Pacific. According to the International Telecommunication Union, mobile broadband penetration in the region reached 78% in 2023, enabling the deployment of telehealth, remote monitoring, and digital case management tools. Countries like Singapore have launched integrated platforms such as HealthHub, which connects patients with medical records, mental health counseling, and caregiver support services. In India, the National Digital Health Mission has linked over 500 million health records as of 2023, creating a foundation for coordinated care. These platforms are increasingly incorporating artificial intelligence to predict care needs and allocate social resources efficiently, improving accessibility and continuity.

Public-Private Partnerships to Expand Community-Based Care Networks

Collaborative models between governments and private entities are emerging as a viable pathway to scale community-oriented health and social services. In Japan, local municipalities have partnered with private firms to operate over 4,000 community integrated care centers, supporting aging-in-place initiatives. These collaborations are increasingly incorporating social impact financing, enabling sustainable scaling of home care, mental health, and disability support services in underserved areas.

MARKET CHALLENGES

Escalating Burden of Non-Communicable Diseases and Mental Health Conditions

The rising prevalence of non-communicable diseases (NCDs) and mental health disorders is placing unprecedented strain on healthcare and social service systems. According to the World Health Organization, NCDs account for 67% of all deaths in the Asia Pacific, with cardiovascular diseases, diabetes, and cancer being the leading causes. In China, over 140 million people live with diabetes, while India reports more than 77 million cases, as per the International Diabetes Federation. Concurrently, mental health conditions are under-addressed. In Indonesia, there are only 0.3 psychiatrists per 100,000 people, severely limiting access to care. Social services are ill-equipped to manage long-term behavioral health needs, and stigma remains pervasive. Without integrated NCD and mental health programs, the burden on families and informal caregivers will continue to grow.

Inequitable Access to Services in Rural and Remote Regions

Geographic and socioeconomic disparities severely limit access to healthcare and social services in rural and remote areas across the Asia Pacific. According to the United Nations, over 1.2 billion people in the region live in rural zones, where health infrastructure is sparse and social workers are scarce. In Papua New Guinea, only 40% of the population lives within a one-hour reach of a health facility, as reported by the National Department of Health. Digital connectivity remains limited. This isolation exacerbates health inequities and delays emergency and preventive interventions, requiring innovative delivery models such as mobile clinics and community health volunteers to bridge the gap.

SEGMENTAL ANALYSIS

By Product and Services Insights

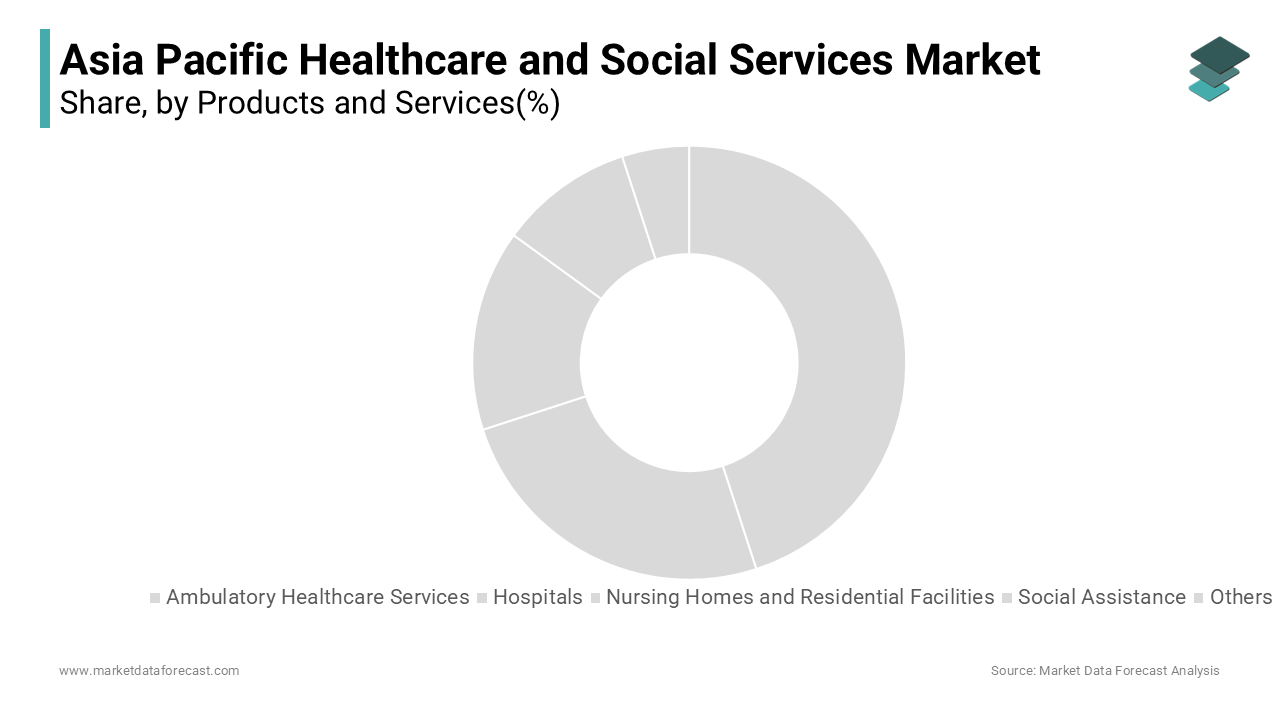

The hospitals segment constituted the largest part of the Asia Pacific healthcare and social services market by accounting for 42.5% of total sector expenditure in 2024. This dominance is primarily driven by the region’s reliance on secondary and tertiary care facilities for diagnosis, treatment, and surgical interventions, particularly in middle- and high-income countries. The segment is further bolstered by rising incidences of complex diseases. Additionally, government investments in healthcare infrastructure have been substantial. India’s Pradhan Mantri Ayushman Bharat Health Infrastructure Mission plans to upgrade 17,788 rural health centers and establish 11 new public health institutes by 2025, reinforcing hospital centrality in national health systems. The concentration of specialized medical personnel and diagnostic technologies within these institutions is a key factor sustaining hospital dominance. Furthermore, insurance reimbursement models in many APAC countries favor inpatient care; for instance, Indonesia’s JKN program reimburses hospital admissions at significantly higher rates than outpatient consultations, incentivizing facility-based treatment. This structural bias, combined with public perception equating hospitals with quality care, ensures continued dominance despite growing emphasis on preventive and community-based models.

The ambulatory healthcare services segment is emerging as the fastest-growing segment in the Asia Pacific market and is projected to expand at a CAGR of 10.8% from 2025 to 2033. This surge is fueled by a strategic shift toward outpatient care, driven by cost efficiency, technological advancements, and policy reforms aimed at reducing hospital overcrowding. In Australia, most medical consultations are conducted in ambulatory settings such as general practitioner clinics and diagnostic centers. The rise of chronic disease management has further accelerated demand. Singapore’s national polyclinic network handles around 6-7 million patient visits annually for diabetes and hypertension monitoring, reducing the burden on acute care facilities. As per the World Health Organization, decentralized care models can lower treatment costs by up to 30% compared to inpatient alternatives. The proliferation of telemedicine and mobile health clinics is a major catalyst for growth. According to the International Telecommunication Union, telehealth consultations in India increased from 5 million in 2020 to over 120 million in 2023, supported by the National Digital Health Mission. Additionally, private equity investment in outpatient chains is rising; India’s Apollo Clinics and Thailand’s Bangkok Hospital Group have expanded into tier-2 and tier-3 cities, offering integrated primary care and diagnostics.

By Type Insights

The public sector remained the leading component of the Asia Pacific healthcare and social services market by commanding an estimated 55.3% share of total expenditure in 2024. This dominance is due to the foundational role of state-funded systems in delivering universal access, particularly in populous nations like China, India, and Indonesia. Governments across the region are expanding infrastructure: China invested a substantial amount in public health facilities between 2020 and 2023. Public systems also administer major social assistance programs. Japan’s Long-Term Care Insurance supports 6.8 million beneficiaries through publicly funded home and institutional care. Public dominance is reinforced by large-scale financing mechanisms and regulatory control. As per the Asian Development Bank, public funding accounts for around 60-70% of total health expenditure in Thailand, Vietnam, and Malaysia, enabling broad service coverage. In Australia, Medicare funds 41% of all health spending, covering physician services, diagnostics, and hospital care for all citizens. The public sector also leads in preventive and community health initiatives: Indonesia’s Posyandu (integrated health posts) network, operated by the Ministry of Health, serves over 30 million people annually in rural areas, delivering maternal care, immunizations, and nutrition support. According to the United Nations, such grassroots programs have contributed to a 35% decline in child mortality across Southeast Asia since 2000. Despite challenges in efficiency, the public sector’s reach and equity mandate ensure its continued centrality.

The private sector is the fastest-growing in the Asia Pacific healthcare and social services market and is expanding at a CAGR of 11.4% from 2025 to 2033. This growth is driven by rising incomes, increasing health insurance penetration, and demand for premium, expedited care. In South Korea, private clinics account for over 80% of outpatient visits, as reported by the Health Insurance Review & Assessment Service, reflecting patient preference for shorter wait times and enhanced service quality. The expansion is particularly pronounced in diagnostic and elective services. As per the International Labour Organization, private social service providers are also gaining traction, particularly in eldercare and mental health, where specialized, fee-based models are filling gaps left by public systems. The surge in private health insurance uptake is a key driver. Besides, foreign direct investment is flowing into private healthcare. The private sector is also pioneering digital health; Singapore’s MyHealth and Indonesia’s Halodoc offer teleconsultations, e-pharmacies, and AI-driven diagnostics, backed by venture capital. As per the World Bank, private providers dominate primary care in urban centers across the region, signaling a structural shift.

REGIONAL ANALYSIS

China Healthcare and Social Services Market Insights

China led the Asia Pacific healthcare and social services market by accounting for 31.5% of total regional expenditure in 2024. The country’s expansive healthcare system is undergoing rapid modernization, driven by national priorities to improve access and quality. As of 2023, China operates over 35,000 hospitals and 1.04 million primary care facilities, serving a population of 1.4 billion, as reported by the National Health Commission. A critical driver is the aging population: by 2035, a notable share of Chinese citizens will be over 60, necessitating expanded geriatric and long-term care services. The integration of AI in diagnostics and the rollout of the National Medical Products Administration’s fast-track approval system have accelerated innovation, positioning China as a regional leader in healthcare transformation.

India Healthcare and Social Services Market Insights

India is also a key player in the Asia Pacific healthcare and social services market. The country’s healthcare landscape is characterized by a dual structure, with public systems serving the majority, while a rapidly expanding private sector caters to urban and insured populations. However, government initiatives like Ayushman Bharat, which have authorized tens of millions of hospital admissions, are improving equity. The social services sector is also evolving, over 1.7 million Accredited Social Health Activists (ASHAs) operate at the community level, as noted by the Ministry of Health, bridging gaps in maternal and child health.

Japan Healthcare and Social Services Market Insights

Japan occupies a strong position in the Asia Pacific healthcare and social services market. The country’s system is distinguished by its integration of medical care and long-term social support, shaped by one of the world’s most aged societies. People aged 65 and over constitute 29.1% of the population, leading to a highly developed network of nursing homes, home-visit care services, and community integrated care centers, as per the Ministry of Health, Labour and Welfare. Japan’s Long-Term Care Insurance system, operational since 2000, covers over 6.8 million enrollees and funds a workforce of 1.8 million certified care workers. The country also leads in health technology adoption.

Australia Healthcare and Social Services Market Insights

Australia holds a significant share of the Asia Pacific healthcare and social services market and is positioning itself as a key player despite its smaller population. The country’s system is renowned for its universal coverage through Medicare, which funds 41% of all health spending and ensures access to medical, diagnostic, and hospital services. Australia also maintains one of the most advanced social service infrastructures in the region, with the National Disability Insurance Scheme (NDIS) supporting over 670,000 participants with personalized care plans, as per the National Disability Insurance Agency. As per the Productivity Commission, over 1.5 million Australians receive formal aged care services annually, with 60% delivered in community settings. Australia’s regulatory rigor and investment in workforce training make it a model for service quality and equity.

South Korea Healthcare and Social Services Market Insights

South Korea is recognized for its high-tech medical infrastructure and rapidly evolving social care policies. The country’s National Health Insurance covers 97% of the population, facilitating access to over 80,000 clinics and 1,000 hospitals, according to the Health Insurance Review & Assessment Service. A defining trend is the surge in demand for long-term care, with 18.4% of the population aged 65 or older in 2023, a figure projected to exceed 30% by 2030. The government launched the Long-Term Care Insurance for the Elderly in 2008, now serving over 1 million beneficiaries. South Korea is also a leader in digital health.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

UnitedHealth Group, AIA Group Limited, China Life Insurance (Overseas) Company Limited, Nippon Life Insurance Company, Dai-ichi Life Holdings, MS&AD Insurance Group Holdings, MetLife Services and Solutions LLC, AXA, Berkshire Hathaway Inc., and Biotricity.

Competition in the Asia Pacific healthcare and social services market is intensifying due to rising demand, policy reforms, and technological disruption. The landscape features a dynamic mix of public institutions, multinational corporations, regional private chains, and digital health startups, each vying for dominance in specialized segments. Unlike in Western markets, competition is not solely driven by scale but by adaptability to local regulatory environments, cultural preferences, and income disparities. Providers differentiating through service quality, digital integration, and patient experience are gaining traction, particularly in urban centers. In rural areas, accessibility and affordability remain decisive factors. The convergence of healthcare and social servicesespecially in aging societies like Japan and South Korea, is creating new battlegrounds for integrated care models. As governments push for universal coverage and digital transformation, firms combining clinical excellence with operational agility are emerging as frontrunners in this complex, high-growth region.

Top Players in the Asia Pacific Healthcare and Social Services Market

Fujifilm Holdings Corporation

Fujifilm has evolved from an imaging company into a major integrated healthcare solutions provider across the Asia Pacific, leveraging its expertise in medical diagnostics, biotechnology, and digital health. The company operates advanced imaging systems, including AI-enhanced mammography and endoscopy equipment, deployed in hospitals throughout Japan, South Korea, Australia, and Southeast Asia. The company has also expanded its regenerative medicine initiatives, commercializing cell processing technologies in collaboration with hospitals in Singapore and Australia. Fujifilm’s strategic focus on precision medicine and point-of-care diagnostics has strengthened its presence in both clinical and preventive care sectors, positioning it as a technology-driven leader in regional healthcare innovation.

Bupa Asia-Pacific

Bupa has established a significant footprint in the Asia Pacific healthcare and social services landscape by delivering private health insurance, direct medical services, and aged care solutions across Australia, Hong Kong, New Zealand, and Vietnam. The organization operates over 600 healthcare facilities, including Bupa Dental Clinics, aged care homes, and outpatient centers, emphasizing integrated care models that bridge insurance and service delivery. The company has also deepened partnerships with public health systems, supporting workforce development and digital record integration. Through its not-for-profit care model in Australia and New Zealand, Bupa delivers person-centered aged care to over 27,000 residents, aligning with regional demands for dignified, long-term social support services.

IHH Healthcare Berhad

IHH Healthcare, headquartered in Malaysia, is one of the largest private healthcare providers in the Asia Pacific, operating a diversified network of hospitals and clinics under brands such as Gleneagles, Pantai, and Mount Elizabeth. With facilities in Malaysia, Singapore, India, and China, the company delivers tertiary care, specialized surgery, and oncology services to a growing middle-class population. The company has also invested in sustainable healthcare infrastructure, opening a green-certified hospital in Hyderabad and upgrading energy systems in Singapore. IHH’s strategic collaborations with academic institutions in Australia and the UK enhance clinical training and research capacity. Its focus on medical tourismserving over 500,000 international patients annuallyfurther solidifies its role as a regional healthcare hub.

Top Strategies Used by the Key Market Participants

Key players in the Asia Pacific healthcare and social services market are deploying multifaceted strategies to consolidate their influence and adapt to evolving demands. A dominant approach is vertical integration, where providers combine insurance, clinical services, and post-acute care under a single ecosystem to improve care continuity and revenue stability. Companies are increasingly investing in digital transformation, adopting AI-driven diagnostics, electronic health records, and telehealth platforms to expand reach and efficiency. Strategic geographic expansion into underserved urban and rural areas is another priority, often supported by public-private partnerships. Leading firms are also forming alliances with technology firms and academic institutions to accelerate innovation in precision medicine and elderly care. Workforce development and localization of care models are critical to ensuring cultural relevance and operational sustainability across diverse populations.

RECENT MARKET DEVELOPMENTS

- In March 2023, Fujifilm launched its AI-powered REiLI diagnostics platform in Thailand and India, enabling real-time detection of gastrointestinal abnormalities and enhancing early intervention capabilities across public and private hospitals.

- In August 2023, Bupa Australia introduced a comprehensive digital health suite integrating teleconsultations, mental health counseling, and chronic care tracking, expanding access for rural and elderly populations.

- In January 2024, IHH Healthcare opened a new 300-bed integrated care facility in Chengdu, China, specializing in oncology and minimally invasive surgery, strengthening its presence in western China.

- In May 2023, Ramsay Health Care acquired two private hospitals in New Zealand, enhancing its surgical and rehabilitation service portfolio in the trans-Tasman region.

- In February 2024, Ping An Good Doctor expanded its telemedicine network into rural Vietnam through a partnership with local clinics, leveraging AI triage to improve primary care access.

MARKET SEGMENTATION

This research report on the Asia Pacific healthcare and social services market is segmented and sub-segmented into the following categories.

By Product and Services

- Ambulatory Healthcare Services

- Hospitals

- Nursing Homes and Residential Facilities

- Social Assistance

- Others

By Type

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

link